Great article from the Center for American Progress on “Corporate Long-Termism, Transparency, and the Public Interest” on moving the XBRL global data standard from financial reporting by public companies to also include sustainability reporting to support climate finance.

The IMA is one of the founding members of the XBRL global data reporting standard to help promote financial and non-financial transparency in both the capital markets and in government reporting by using a machine-readable format for better data analytics.

It only makes sense that as the US SEC moves closer to sustainability reporting by public companies Inline XBRL be extended beyond the financial data that is tagged in XBRL to sustainability disclosed data for public disclosure. Bu linking both we also move closer to Integrated Reporting by linking climate finance data to financial data to improve a company’s investment alpha and shift trillions of dollars in investor funds around the world to reward companies moving forward in development of new sustainability technologies and energy sources to avoid global warming.

According to the report:

Boosting transparency on environmental, social, and governance matters can help align the interests of investors, management, and the public towards shared long-term success.

The SEC’s 2016 Concept Release on Regulation S-K—the principal SEC regulation that governs corporate disclosure—garnered more than 26,500 comments from investors and the public. An analysis of these commenters showed that the comments overwhelmingly and persuasively favored ESG disclosures across a wide range of issues.11

WHAT IS SUSTAINABILITY REPORTING?

ITS GOOD BUSINESS

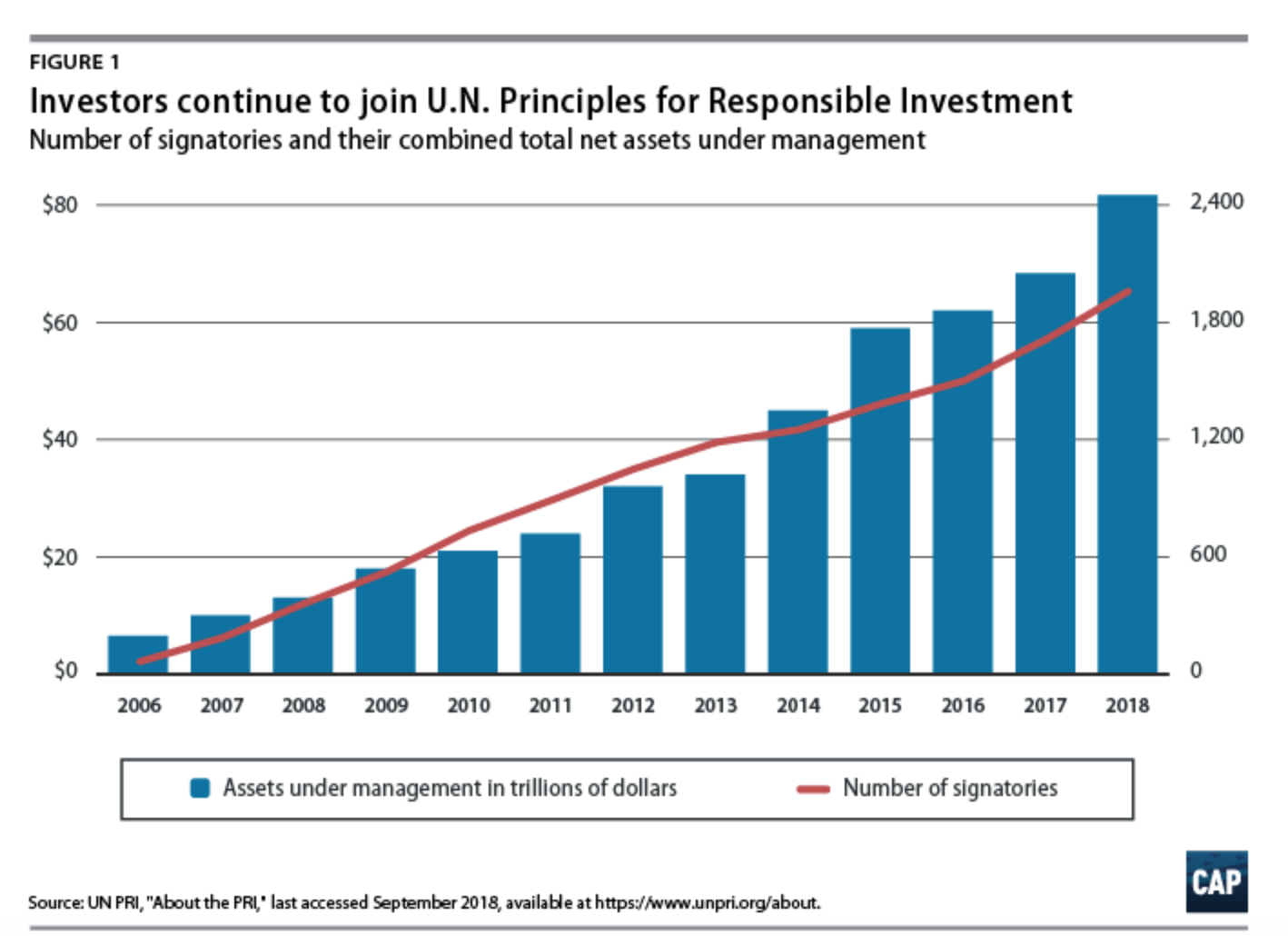

Investors of all types increasingly recognize that ESG information is an essential part of evaluating potential investments. A recent study found that 82 percent of mainstream, or non-ESG focused, investors considered ESG information when making investment decisions.28 Moreover, at more than $8.72 trillion in total assets under management as of 2014, investing that takes into account ESG criteria is no longer a niche investment category.29 The extraordinary increase in the number of signatories to the Principles for Responsible Investment (PRI) makes this clear. The PRI is a network of investors focused on promoting responsible investment through understanding and incorporating ESG factors into investment decision-making. Since its launch by the United Nations in 2006 with just 100 members, the PRI now has more than 1,800 signatories who manage more than $80 trillion in assets.

REGARDLESS OF THE US SEC COMPANIES ARE DISCLOSING SUSTAINABILITY INFORMATION TO WORLDWIDE INVESTORS:

According to the Governance and Accountability Institute, the number of S&P 500 companies making “sustainability reports” increased from less than 20 percent in 2011 to more than 85 percent in 2017.37

CLIMATE CHANGE FINANCIAL IMPACT CONTINUES TO GROW AROUND THE WORLD

A 2015 estimate of value-at-risk (VaR) associated with climate change by The Economist found that expected losses to the private sector from a warming planet could amount to $4.2 trillion by 2100, discounted in present value terms.60 As the publication notes, this is approximately the same size as Japan’s entire annual gross domestic product (GDP) or as the total value of all the world’s listed oil and gas companies.61 The Economist also analyzes the risk of a 5-degree or 6-degree warming scenario and finds private sector losses ranging from $7 trillion to nearly $14 trillion, respectively.62 Public sector costs would add an additional $43 trillion in estimated losses over the next 80-plus years.63 Focusing specifically on U.S. publicly listed companies, climate risks to corporate America are widespread.64 One estimate finds that the overall market cap of affected assets is $27.5 trillion, which is 93 percent of the U.S. equity market value.65

USING XBRL FOR BETTER SUSTAINABILITY DATA ANALYTICS

The SEC should also require that data for all corporate filings, including ESG information, be provided to investors in a machine-readable—or “structured data”—format embedded directly in the disclosure document, known as Inline eXtensible Business Reporting Language (Inline XBRL) and subject to the same level of audit and accountability as any filing.176 This would be an extension of the SEC’s rule, finalized in 2018, that requires financial information be provided via Inline XBRL.177 Utilizing an Inline XBRL format reduces the cost to investors of accessing data and increases its reliability, as it promises to reduce the incidence of errors compared to when structured data is provided as a separate attachment.178

IMA AND CORPORATE SUSTAINABILITY REPORTING USING THE XBRL DATA STANDARD FOR BETTER ANALYTICS

Stay tuned as we report on progress by the US Securities & Exchange Commission on this topic of corporate sustainability reporting and the use of technologies like XBRL to enhance machine-readability of disclosed data and data analytics.

Given the rising demand for sustainability performance data to support internal and external decision making in creating, growing and reporting value, the paper asserts that confidence in this type of information is strengthened by the application of the COSO ICIF, a robust and globally recognized framework designed to apply to both financial and non-financial information.

Former FASB Chairman Robert Herz, IMA (Institute of Management Accountants) President and CEO Jeff Thomson, and sustainability reporting expert Brad Monterio of Colcomgroup, today released a jointly authored thought paper, "Leveraging the COSO Internal Control – Integrated Framework (ICIF) to Improve Confidence in Sustainability Performance Data." These controls will be necessary as companies move forward with sustainability reporting and XBRL can be used on data that is disclosed to the capital markets to enhance data analytics and integrated reporting with the corporate financial data disclosed.

Meanwhile, hear more about what the Japanese Ministry of Environment is doing related to ESG disclosures in Japan based on Corporate XBRL filings at the upcoming DATA AMPLIFIED CONFERENCE in Dubai on November 13-15, 2018.

The MoE project is explicitly focussed on providing *long term investors* with insight into the ESG factors that provide opportunities and represent challenges for these firms. In turn, this promotes integrated thinking.

NAOMI SUGO Ministry of the Environment of Japan will be speaking on Environmental Information Disclosures with XBRL at the upcoming DATA AMPLIFIED CONFERENCE IN DUBAI. The Ministry of the Environment of Japan has promoted environmental conscious activities by companies through information disclosure, for example, by preparing guidelines for environmental reporting that includes using XBRL for better transparency and accountability.

The IMA is an Association Partner at DATA AMPLIFIED CONFERENCE and IMA members get a discount if they attend and can ask questions of Naomi and other key XBRL leaders and regulators around the world including Louis Matherne with the US Financial Accounting Standards Board (FASB) - the keeper of the XBRL taxonomy used by US public companies by the US Securities and Exchange Commission.

To register for DATA AMPLIFIED CONFERENCE please click on this link